You’ve seen the ads with Ice-T. You’ve heard the promises of protection from costly, unexpected car repairs. But you’ve also likely seen the warnings, the mixed reviews, and the headlines about lawsuits. So, is CarShield a smart financial shield for your car, or is it a high-cost gamble?

For a specific type of driver—typically with an older, high-mileage vehicle outside its factory warranty—a CarShield extended warranty review shows it can offer a degree of peace of mind. However, for many others, it’s a costly service that may never pay for itself. This 2026 review cuts through the marketing noise to give you a straight answer, breaking down the math to help you decide if the CarShield pros and cons make it right for you.

What Is CarShield and How Does It Actually Work?

First, it’s crucial to understand that CarShield is not car insurance. It is a Vehicle Service Contract (VSC) provider. While car insurance covers damage from accidents, theft, and other external events, a VSC covers the cost of repairs for mechanical failures. Think of it as a health plan for your car’s engine, transmission, and other vital parts.

The business model can be a source of confusion. CarShield acts as a broker, marketing and selling these service contracts to consumers. However, the entity responsible for handling claims and paying repair shops is usually a separate third-party administrator, most often a company called American Auto Shield. This is a critical point to remember when considering if CarShield is legit.

When a covered breakdown occurs, your interaction is not with CarShield, but with the administrator. The process generally involves you paying a deductible (typically between $100 and $500), after which the administrator pays the ASE-certified repair facility directly for the covered portion of the bill.

The Break-Even Math: When Does CarShield Pay for Itself?

To determine if CarShield is financially sensible, you must start with a simple break-even analysis. With the CarShield cost averaging around $140 per month, the annual expense for a plan is approximately $1,680. This figure is the foundation of your decision.

The core question you must ask is straightforward: Do you realistically expect to face more than $1,680 in covered repair costs within the next year? If the answer is no, you will have spent more on the contract than you received in benefits.

| Monthly Premium | Annual Cost | Break-Even Repair Bill |

|---|---|---|

| $120 | $1,440 | > $1,440 |

| $140 | $1,680 | > $1,680 |

| $160 | $1,920 | > $1,920 |

This calculation doesn’t even factor in your deductible, which you would have to pay on top of the premium for each repair claim. If a covered repair costs $2,000 and your deductible is $200, the plan saves you $1,800. If your annual premium was $1,680, you’ve come out ahead by just $120. This highlights the narrow financial window where a VSC provides a clear monetary advantage.

CarShield Plans and Cost: What’s Actually Covered?

CarShield offers a tiered system of plans, each designed for different vehicle types and coverage needs. While the specifics can vary, they generally follow a pattern from basic powertrain protection to more comprehensive, exclusionary coverage. The most common plans are Diamond and Platinum, which are promoted as the most comprehensive options.

| Plan Tier | General Coverage Focus |

|---|---|

| Diamond | Exclusionary (bumper-to-bumper style), covering most vehicle components except for a short list of exclusions. |

| Platinum | Comprehensive coverage for high-mileage vehicles, including the engine, transmission, AC, and electrical systems. |

| Gold | Enhanced powertrain coverage that adds components like the alternator, starter, and power windows. |

| Silver | Basic powertrain coverage, focusing on the engine, transmission, and water pump. |

| Aluminum | Specialty coverage for electrical and computer systems, often for modern, tech-heavy vehicles. |

Monthly costs typically range from $99 to over $170, with the final price depending on your vehicle’s make, model, age, and mileage. Deductibles also vary, commonly set at $100, but options can range from $0 to $500. A higher deductible will generally result in a lower monthly premium.

Crucially, all plans have exclusions. No VSC covers everything. Common items not covered by CarShield include routine maintenance like oil changes and brake pads, pre-existing conditions that were present before you purchased the plan, cosmetic damage, and any failures resulting from accidents, neglect, or unauthorized modifications.

The Red Flags: FTC Settlement, BBB Complaints, and Claims Process

While CarShield is a legitimate company, it operates under a cloud of significant consumer complaints and regulatory scrutiny. In 2024, the company agreed to a $10 million settlement with the Federal Trade Commission (FTC) over charges of deceptive advertising and making misleading statements to consumers. This action suggests a history of aggressive sales tactics that may have overstated the benefits of their plans.

Furthermore, there is a notable paradox in CarShield’s public ratings. The company holds a high rating (often A or A+) from the Better Business Bureau (BBB). However, this rating primarily reflects the company’s responsiveness in addressing filed complaints, not the absence of them. On the same platform, CarShield has thousands of negative customer reviews, creating a confusing picture for consumers wondering if CarShield is a scam.

The most persistent issue stems from the claims process. Because claims are handled by a third-party administrator like American Auto Shield, customers can find themselves in a frustrating loop. If a claim is denied, CarShield may direct the customer to the administrator, who may in turn find a clause in the fine print to justify the denial. This two-company structure can make it difficult to get a clear resolution.

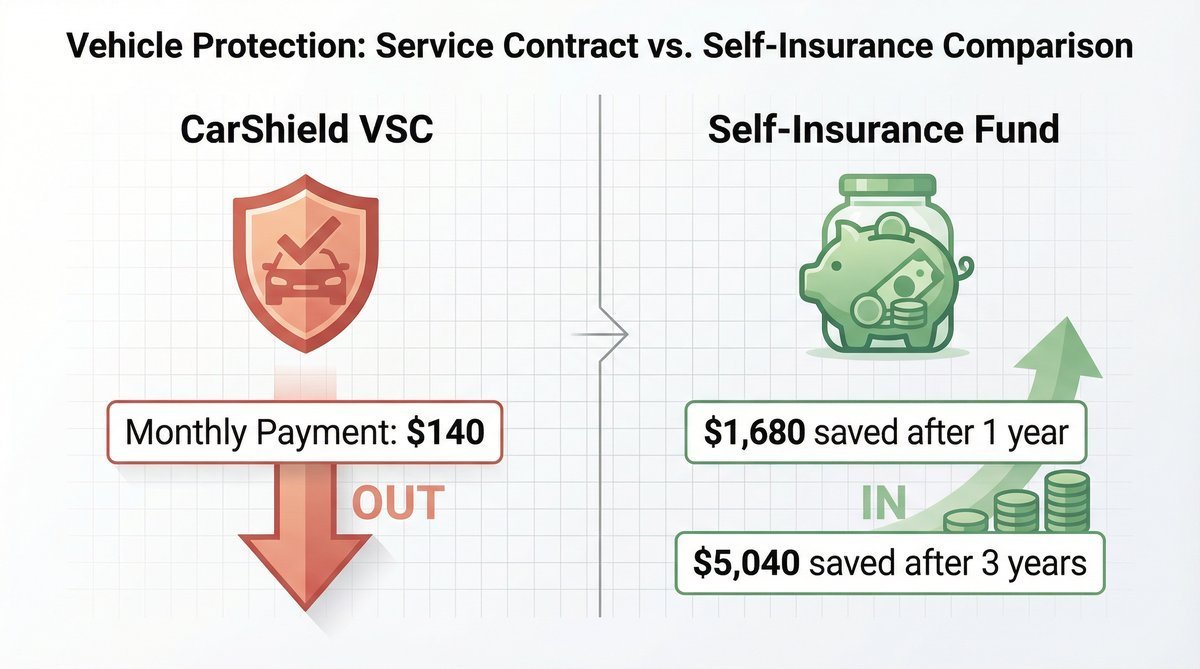

CarShield vs. a Savings Account: The Self-Insurance Alternative

One of the most compelling arguments against any VSC is the self-insurance strategy. Instead of paying CarShield approximately $140 per month, you could deposit that same amount into a dedicated high-yield savings account for car repairs. In one year, you would have saved over $1,680, plus interest.

This approach has significant advantages. If your car remains trouble-free, that money is still yours. You have complete control over it and can use it for any purpose. This CarShield vs. saving money for car repairs comparison also eliminates the risk of a claim being denied or dealing with a difficult claims administrator.

The primary risk of self-insuring is being hit with a major, unexpected repair bill that exceeds your savings. A complete engine or transmission failure can cost several thousand dollars. A VSC is essentially a bet that you will face such a catastrophic failure, while self-insuring is a bet that you won’t, or that you can cover it if you do.

Who Should Get CarShield (and Who Should Absolutely Avoid It)

Not everyone is a suitable candidate for a Vehicle Service Contract. The decision to purchase a plan like CarShield should be based on your specific vehicle profile and financial situation.

A VSC might be a good option for owners of older, high-mileage vehicles. If your car is between 5 and 10 years old with over 80,000 miles, it is statistically more likely to experience a major mechanical failure. A VSC can provide a safety net against these age-related risks, making it potentially worth it for high-mileage vehicles. Similarly, if a sudden, unexpected repair bill of $2,000 or more would be financially devastating, the predictable monthly payment of a VSC can offer valuable peace of mind and budget stability.

On the other hand, there are several profiles who should likely avoid CarShield. If your vehicle is still covered by its original factory warranty, or if it is a model known for its exceptional reliability (like many Toyotas or Hondas), a VSC is likely an unnecessary expense. Likewise, if you have a healthy emergency fund and can comfortably absorb a $3,000+ repair bill without financial strain, the self-insurance strategy is almost always the more prudent financial choice. CarShield also does not offer plans in California due to the state’s strict regulatory requirements for service contracts.

CarShield vs. The Competition (Endurance & Carchex)

CarShield is not the only player in the VSC market. Its primary competitors, Endurance and Carchex, offer different models that may be more appealing to certain consumers.

| Feature | CarShield | Endurance | Carchex |

|---|---|---|---|

| Provider Type | Broker | Direct Provider | Broker |

| BBB Rating | A+ | A+ | A+ |

| Unique Feature | Heavy advertising, celebrity endorsements | Handles claims directly, simplifying the process | Highly rated customer service and plan variety |

| Best For | Budget-conscious buyers looking for low monthly payments | Consumers who want a simpler, direct claims process | Buyers who prioritize customer service and support |

When comparing CarShield vs. Endurance, the main difference is that Endurance is a direct provider. This means the company that sells you the plan is the same one that administers claims, which can lead to a more streamlined and less contentious claims process. Carchex, like CarShield, is a broker, but it has built a strong reputation for excellent customer service and transparency.

The Verdict: Is CarShield Worth It in 2026?

After a thorough analysis, the verdict is clear: CarShield is a financial tool with a very specific use case. It is not a scam, but its value is highly dependent on your personal situation, vehicle’s condition, and tolerance for risk. For most drivers, especially those with reliable cars or adequate savings, the math does not add up.

The self-insurance strategy—saving the monthly premium in a dedicated fund—is financially superior for the majority of people. It offers more control, flexibility, and a better long-term return.

However, if you own an aging, high-mileage vehicle prone to costly breakdowns and lack the cash reserves to handle a sudden, multi-thousand-dollar repair bill, CarShield can serve as a viable, albeit imperfect, safety net. It transforms an unknown, potentially catastrophic expense into a predictable, manageable monthly payment.

Frequently Asked Questions (FAQ) About CarShield

Is CarShield a rip-off?

CarShield is a legitimate company, not a rip-off. However, its business model, reliance on third-party administrators, and history of FTC complaints for deceptive advertising mean that consumers should approach with caution and read their contracts carefully.

Does CarShield really pay for repairs?

Yes, CarShield does pay for covered repairs. The key phrase is “covered repairs.” Many customer complaints stem from claims being denied because the specific part or failure type was listed as an exclusion in the contract’s fine print.

What are the biggest complaints about CarShield?

The most common complaints involve denied claims, misleading sales tactics, and difficulty canceling plans. The complex relationship between CarShield (the seller) and American Auto Shield (the claims administrator) is a frequent source of customer frustration.

Can I cancel my CarShield plan?

Yes, you can typically cancel your CarShield plan. Most contracts offer a pro-rated refund for the unused portion of the contract, though cancellation fees may apply.

Is CarShield better than Endurance?

Many industry experts prefer Endurance because it is a direct provider, which can simplify the claims process. However, CarShield may offer lower monthly premiums, making it more attractive to budget-conscious consumers.

Why is CarShield not available in California?

California has some of the strictest consumer protection laws in the country regarding vehicle service contracts. CarShield’s business model and contract terms do not currently meet these stringent regulatory requirements.