FHA mortgage requirements are designed to make homeownership more accessible, particularly for first-time buyers or those with less-than-perfect credit. These loans, insured by the Federal Housing Administration, offer flexible qualification criteria compared to conventional mortgages. Understanding the specific guidelines for credit scores, down payments, debt-to-income ratios, and property standards is crucial for applicants seeking to secure an FHA-insured loan.

What is an FHA Mortgage?

An FHA mortgage is a home loan insured by the Federal Housing Administration, a division of the U.S. Department of Housing and Urban Development (HUD), designed to help individuals achieve homeownership by reducing the risk for lenders.

The Federal Housing Administration (FHA) does not directly lend money for home purchases. Instead, it insures mortgages issued by FHA-approved private lenders, such as banks and credit unions. This insurance protects lenders from losses if a borrower defaults on their loan, which in turn encourages them to offer more favorable terms, including lower down payments and more flexible credit score requirements, to a broader range of applicants. Established in 1934, the FHA’s primary goal is to stabilize the housing market and expand homeownership opportunities across the nation.

Credit Score Requirements for FHA Loans

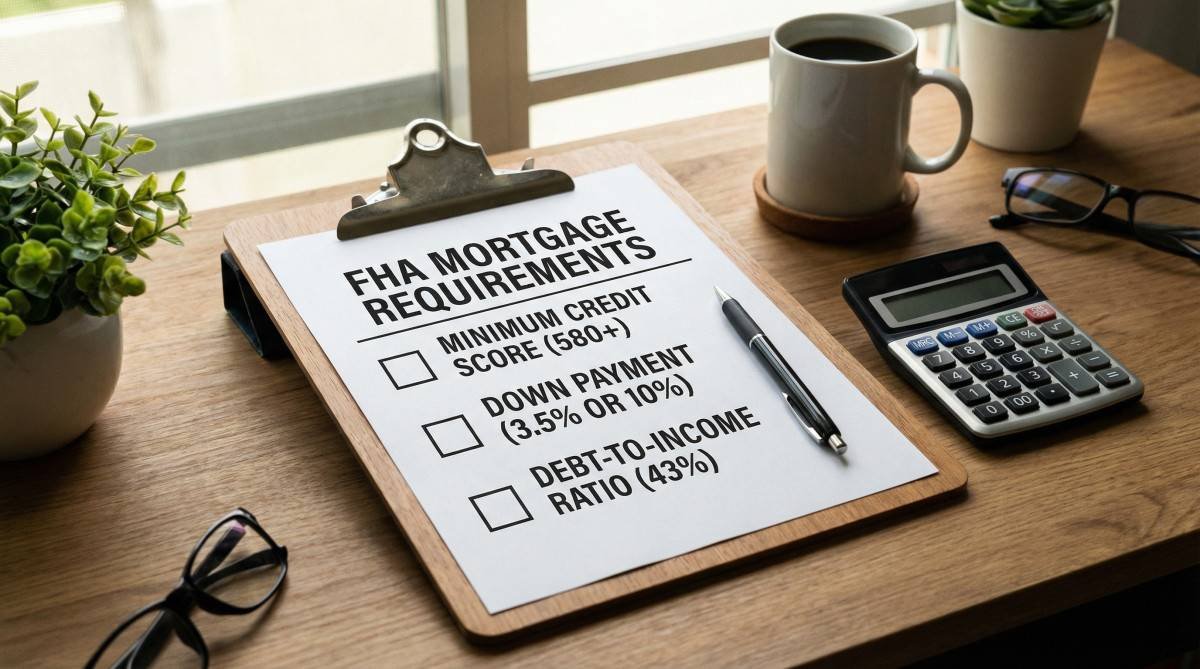

FHA loan applicants typically need a minimum FICO score of 580 to qualify for the lowest down payment option, though scores as low as 500 may be accepted with a higher down payment.

The FHA sets baseline credit score guidelines, but individual lenders may impose their own, often higher, minimums. For borrowers with a FICO score of 580 or higher, the minimum down payment required is 3.5% of the home’s purchase price. If a borrower’s FICO score falls between 500 and 579, a higher down payment of 10% is generally required. A strong credit history demonstrates a borrower’s reliability in managing financial obligations, which can also lead to more favorable interest rates and loan terms. Lenders evaluate the overall credit profile, including payment history, outstanding debts, and length of credit history, to assess risk.

Down Payment and Closing Cost Guidelines

FHA loans offer flexible down payment options, with a minimum of 3.5% for eligible borrowers, and allow certain closing costs to be financed or covered by approved sources.

The minimum down payment for an FHA loan is 3.5% for borrowers with a credit score of 580 or above. For those with credit scores between 500 and 579, a 10% down payment is required. These funds can come from various approved sources, including personal savings, gifts from family members, or down payment assistance programs. Gift funds must be properly documented with a gift letter from the donor, explicitly stating that the funds are not a loan and require no repayment. Closing costs, which typically range from 2% to 5% of the loan amount, can include appraisal fees, title insurance, and origination fees. FHA guidelines permit sellers to contribute up to 6% of the sales price towards a buyer’s closing costs, and some costs can be rolled into the loan amount, reducing upfront expenses for the borrower.

Debt-to-Income Ratio Explained

The debt-to-income (DTI) ratio is a key FHA requirement that assesses a borrower’s ability to manage monthly payments, typically preferring a ratio of 43% or less.

The debt-to-income (DTI) ratio is a critical factor in determining loan eligibility. It is calculated by dividing a borrower’s total monthly debt payments by their gross monthly income. The FHA generally looks for a DTI ratio of 43% or less, though in some cases, with strong compensating factors such as significant cash reserves or a higher credit score, a DTI up to 50% may be accepted. Lenders consider two types of DTI: the

front-end DTI (housing expenses only) and the back-end DTI (housing expenses plus all other monthly debt obligations). A lower DTI indicates a greater capacity to handle additional debt, making the borrower a less risky candidate for a mortgage.

Income and Employment Verification

FHA loan applicants must demonstrate a stable employment history, typically for at least two years, and provide verifiable income documentation to ensure repayment capability.

To qualify for an FHA loan, borrowers must provide evidence of stable and reliable income. This typically involves a two-year employment history with consistent earnings. Lenders will request documentation such as W-2 forms, pay stubs, and federal tax returns for the past two years. For self-employed individuals, a more extensive review of business financial statements and tax returns will be conducted to assess income stability. The FHA does not impose specific income limits, but the income must be sufficient to cover the mortgage payments and other monthly obligations, as determined by the DTI ratio. Any gaps in employment or significant changes in income may require additional explanation and documentation.

Property Eligibility and Appraisal Standards

FHA-insured properties must meet specific eligibility criteria, including being a primary residence and passing an FHA appraisal to ensure they meet minimum health, safety, and structural standards.

The property being financed with an FHA loan must be the borrower’s primary residence and cannot be an investment property or a second home, with exceptions for multi-unit dwellings where the borrower occupies one unit. All properties must undergo an FHA appraisal conducted by an FHA-approved appraiser. This appraisal not only determines the property’s market value but also ensures it meets the FHA’s Minimum Property Standards (MPS), which cover health, safety, and structural integrity. These standards are designed to protect both the borrower and the FHA. FHA loan limits vary by county and are updated annually, reflecting the median home prices in those areas. Borrowers must ensure the loan amount does not exceed the FHA limit for their specific county.

Mortgage Insurance Premiums (MIP)

FHA loans require both an Upfront Mortgage Insurance Premium (UFMIP) and an Annual Mortgage Insurance Premium (MIP) to protect lenders against potential losses from borrower default.

A key component of FHA loans is the requirement for mortgage insurance. This includes two parts: an Upfront Mortgage Insurance Premium (UFMIP) and an Annual Mortgage Insurance Premium (MIP). The UFMIP is a one-time charge equal to 1.75% of the loan amount, which can be paid at closing or financed into the loan. The annual MIP is paid monthly and its amount varies based on the loan-to-value (LTV) ratio, loan term, and original loan amount. For most FHA loans with a down payment of less than 10%, the MIP is required for the entire life of the loan. If the down payment is 10% or more, the MIP is typically required for 11 years. These premiums contribute to the FHA’s mutual mortgage insurance fund, which safeguards lenders.

FHA Loan Requirements Summary Table

| Requirement Category | General FHA Guideline | Key Details |

|---|---|---|

| Credit Score | 500-579 FICO: 10% down payment 580+ FICO: 3.5% down payment | Lenders may have higher minimums; strong credit can lead to better terms. |

| Down Payment | Minimum 3.5% | Can be sourced from savings, gifts, or assistance programs; must be documented. |

| Debt-to-Income (DTI) Ratio | Typically 43% or less | Up to 50% possible with strong compensating factors. |

| Employment History | Stable for at least two years | Verifiable income through W-2s, pay stubs, tax returns. |

| Property Type | Primary residence | Must pass FHA appraisal for Minimum Property Standards. |

| Mortgage Insurance | UFMIP (1.75%) and Annual MIP | Annual MIP duration depends on down payment amount. |

Common FHA Loan Misconceptions

| Misconception | Factual Clarification |

|---|---|

| FHA lends money directly. | The FHA insures loans made by approved private lenders, it does not lend money itself. |

| FHA loans are only for first-time homebuyers. | While popular with first-time buyers, FHA loans are available to any eligible borrower, not just those purchasing their first home. |

| Any property qualifies for an FHA loan. | Properties must meet FHA Minimum Property Standards and pass an FHA appraisal. |

| FHA loans have strict income limits. | There are no specific income limits; rather, income must be stable and sufficient to meet debt obligations. |

Frequently Asked Questions

Q1: What is the minimum credit score for an FHA loan?

A: A minimum FICO score of 580 is generally required for a 3.5% down payment, while a score between 500 and 579 may require a 10% down payment.

Q2: How much is the down payment for an FHA mortgage?

A: The down payment can be as low as 3.5% for borrowers with a credit score of 580 or higher, or 10% for scores between 500 and 579.

Q3: Are there income limits for FHA loans?

A: The FHA does not impose specific income limits, but borrowers must demonstrate stable and verifiable income to support the mortgage payments.

Q4: What is the debt-to-income ratio for an FHA loan?

A: Typically, the FHA prefers a debt-to-income ratio of 43% or less, though exceptions can be made with compensating factors.

Q5: Do FHA loans require mortgage insurance?

A: Yes, FHA loans require both an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP).

Conclusion

FHA loans serve as a vital pathway to homeownership for many individuals and families, offering more flexible qualification criteria than conventional mortgages. By understanding and meeting the specific FHA mortgage requirements related to credit scores, down payments, debt-to-income ratios, and property standards, prospective homebuyers can navigate the process with greater confidence. These government-insured loans are particularly beneficial for those with moderate incomes or less-than-perfect credit histories, providing an opportunity to achieve the dream of owning a home. Exploring FHA options with an approved lender can be a crucial first step towards securing affordable and accessible home financing.