Shared ownership is worth it — but only if three factors align for you: a genuine affordability gap that makes full ownership unreachable right now, long-term plans stable enough to justify the costs of buying and eventually staircasing, and a local market where the scheme’s restrictions won’t trap you on the way out. Miss any one of those, and the maths can turn against you quickly.

The scheme itself is straightforward enough: a buyer purchases a share of a property — typically between 10% and 75% — from a housing association, pays a mortgage on that share, and pays subsidised rent on the portion the housing association retains. Simple in theory. Considerably more complicated in practice.

For first-time buyers priced out of full ownership in London or the South East, shared ownership can be a genuine ladder onto the property market. For others — those with flexible timelines, uncertain income, or plans to move within a few years — the hidden costs, service charge obligations, and resale restrictions can make it an expensive detour. The real numbers, the genuine risks, and the alternatives all matter — and they all point in different directions depending on where you live and how long you plan to stay.

How Shared Ownership Actually Works

Shared ownership means buying between 10% and 75% of a property from a housing association, paying a mortgage on that share, and paying subsidised rent on the remainder — all under a leasehold arrangement that makes the housing association both co-owner and landlord simultaneously.

The split between your share and the housing association’s share

Buyers purchase their chosen share from a housing association — organisations such as Clarion Housing or Peabody — and take out a standard repayment mortgage on that portion alone. Rent on the remaining share is set below market rate, typically around 2.75% of the unsold equity per year, though this figure varies by provider. Crucially, “owning” a share is not the same as owning the property outright: the housing association remains a co-owner and landlord simultaneously.

Staircasing — buying more over time

Staircasing is the process of purchasing additional shares in your property incrementally, with the goal of eventually reaching 100% ownership. Each new tranche is priced at current market value at the time of purchase — not the price you originally paid. That means if property values rise significantly between tranches, each step up the ladder costs more, and the total amount paid to reach full ownership can substantially exceed the original property price.

| Share Purchased | What You Pay | To the Housing Association |

|---|---|---|

| Your share (10–75%) | Mortgage repayments | — |

| Remaining share | Subsidised rent (~2.75% p.a. of unsold equity) | Monthly rent payment |

| Additional tranches (staircasing) | Mortgage on new share at current market value | Reduced rent as share grows |

The Real Monthly Cost — Renting vs. Shared Ownership vs. Full Ownership

For a £280,000 property, shared ownership typically produces a total monthly outgoing of roughly £950–£1,100 — more than renting in some markets, less than full ownership in high-cost areas, but with one critical difference: part of that payment is building equity. The numbers below make that comparison concrete.

What goes into your monthly shared ownership bill

Four separate line items land on a shared ownership buyer’s doorstep every month. First, a mortgage repayment covering only the purchased share. Second, subsidised rent paid to the housing association on the share they still own — typically set at around 2.75% of the unsold share’s value annually, though this figure varies by provider. Third, a service charge for communal maintenance, which is a leasehold obligation and can rise year-on-year with little warning. Fourth, a buildings insurance contribution, usually collected alongside the service charge by the housing association.

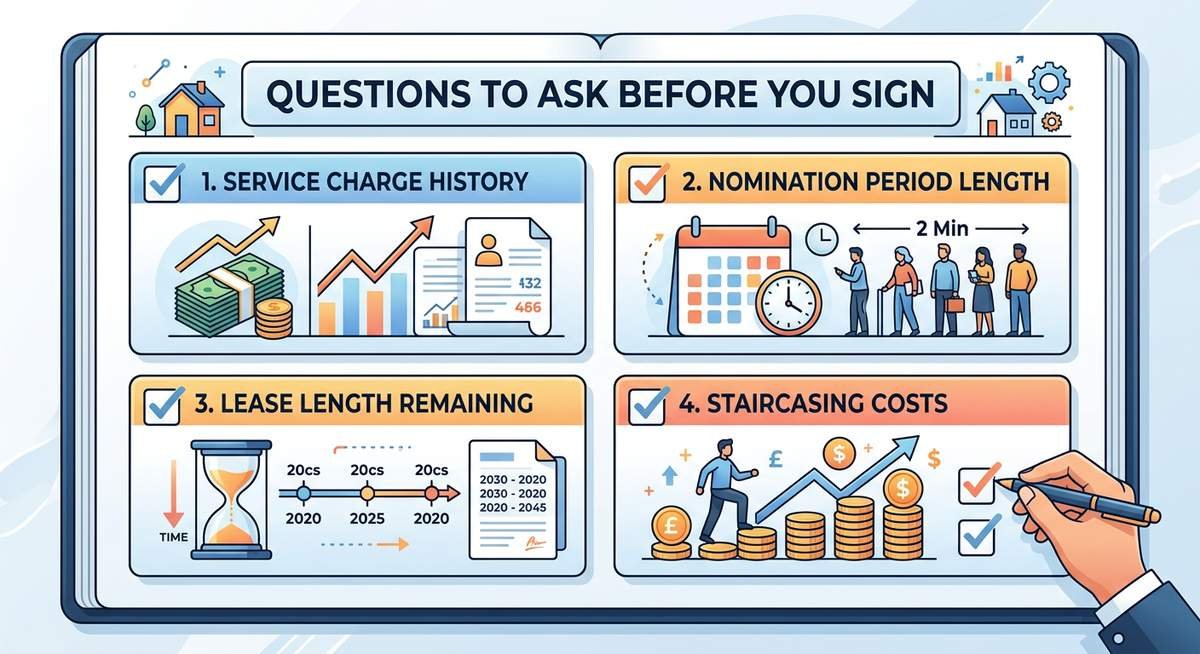

Service charges deserve particular attention. Unlike a mortgage payment, which is fixed or tracker-linked, service charges are set unilaterally by the housing association and have no statutory cap. Buyers should always request at least three years of historical service charge accounts before exchanging contracts.

Side-by-side cost table for a £280,000 property

The worked example below uses a 25% share purchase on a £280,000 flat — a common entry point. The shared ownership deposit is £3,500 (5% of the £70,000 share), leaving a mortgage of £66,500. Full ownership assumes a 10% deposit (£28,000) and a mortgage of £252,000. Private rent is based on a typical market rate for an equivalent flat. Mortgage figures use an indicative 5.0% repayment rate over 25 years.

| Cost Component | Shared Ownership (25% share) | Private Renting | Full Ownership (10% deposit) |

|---|---|---|---|

| Mortgage repayment | ~£390/month | — | ~£1,476/month |

| Rent to housing association | ~£481/month | — | — |

| Private rent | — | ~£1,200/month | — |

| Service charge | ~£150/month | — | ~£150/month (if leasehold) |

| Buildings insurance contribution | ~£20/month | — | ~£25/month |

| Estimated monthly total | ~£1,041 | ~£1,200 | ~£1,651 |

| Equity built each month | Partial (on 25% share) | None | Full |

| Deposit required | £3,500 | ~£2,400 (2 months) | £28,000 |

Figures are illustrative. Actual costs vary by region, lender rate, and housing association. Rent to housing association calculated at approximately 2.75% per annum on the unsold 75% share (£210,000).

The headline finding: shared ownership undercuts full ownership by around £610 per month on these assumptions, while costing roughly £160 less than private renting. The deposit gap is the starkest number — £3,500 versus £28,000. Staircasing over time can shift the balance further toward full ownership, but each additional tranche is priced at current market value, so a rising property market increases the cost of buying out the housing association’s remaining share.

The Genuine Pros — When Shared Ownership Makes Sense

Shared ownership delivers genuine value in one specific scenario: you have a stable income, a small deposit, and you live somewhere that has priced you out of full ownership entirely. For that buyer, the scheme is not a compromise — it is the only realistic route onto the ladder.

A lower deposit barrier in high-cost areas

Because the deposit is calculated on your purchased share rather than the full property value, the numbers shift dramatically in your favour. On a £280,000 flat, buying a 25% share means your 5% deposit is £3,500 — not £14,000. In London and the South East, where that same property might be worth £450,000, the difference between shared ownership and full ownership can represent years of additional saving.

Eligibility is capped at a £90,000 household income in London and £80,000 across the rest of England, which means the scheme is genuinely targeted at middle-income buyers rather than those who simply prefer a smaller outlay.

Building equity while you live there

Renting builds nothing. Every month of private rent is money that leaves your balance sheet permanently. Even a 25% share in a housing association property participates in capital growth — if the property rises in value, your share rises with it.

Disciplined staircasing amplifies this further. Buying additional tranches over time — say, moving from 25% to 50% to 75% — converts monthly rent payments into owned equity. According to Homes England, staircasing to 100% ownership is possible on most shared ownership properties, making full freehold ownership a realistic long-term destination rather than a theoretical one.

The Real Risks — Hidden Costs and Exit Traps

Shared ownership carries three financial risks that are routinely underplayed: escalating service charges you have no power to control, repair liabilities that fall entirely on you despite partial ownership, and a resale process that can leave you waiting months for a buyer from a restricted pool. Understanding these before you sign is not pessimism — it’s basic due diligence.

Service charges and who pays for repairs

As a leaseholder, you are liable for 100% of repair and maintenance costs on your individual property — even if you own only 25% of it. The housing association owns the remaining share but carries none of the day-to-day repair burden inside your home. That asymmetry surprises a significant number of buyers.

Service charges for communal areas — lifts, grounds, building insurance — are set unilaterally by the housing association and can rise year on year without your approval. Charges on new-build leasehold flats have increased sharply in recent years, with some buyers facing annual bills exceeding £3,000 on top of mortgage and rent payments. The Leasehold Advisory Service (LEASE) confirms that shared ownership leaseholders have the same right to challenge unreasonable service charges as any other leaseholder, but the process is time-consuming and not guaranteed. Always request at least three years of historical service charge accounts before exchanging contracts.

Selling a shared ownership property is harder than you think

Selling is where the “trapped owner” narrative has real substance. Most shared ownership leases include a nomination period — typically eight weeks — during which the housing association has the exclusive right to find a buyer before the property reaches the open market. If the housing association fails to source a buyer within that window, you can list publicly, but your buyer must still qualify for the scheme.

That restricted buyer pool — limited to people who meet shared ownership eligibility criteria — is meaningfully smaller than the general market. A smaller pool means less competition, which can suppress your eventual sale price and extend time on market well beyond what you’d expect selling a standard freehold property.

Can you lose money on shared ownership?

Yes. Three scenarios create genuine financial loss: property values fall and your equity shrinks; service charges escalate to the point where total monthly outgoings exceed comparable private rent; or you are forced to sell during the nomination period at a price dampened by the restricted buyer pool. None of these is hypothetical.

| Risk Factor | Shared Ownership | Full Ownership | Renting |

|---|---|---|---|

| Property value falls | Equity loss on owned share | Equity loss on full value | No exposure |

| Service charge rises | Full liability, no control | Freehold: no charge (usually) | Landlord absorbs it |

| Forced sale | Nomination period restricts buyers | Open market, full buyer pool | Give notice and leave |

| Zero equity outcome | Possible if costs erode gains | Possible in falling market | Guaranteed — no equity built |

Context matters here. Full ownership carries identical market risk on a much larger capital sum. Renting guarantees zero equity regardless of market conditions. Shared ownership sits between those two positions — but only if the numbers actually work in your specific area, and only if you go in clear-eyed about the staircasing costs you’ll face when property values have risen.

Is Shared Ownership Worth It for First-Time Buyers?

For first-time buyers specifically, shared ownership is worth considering when a full mortgage is out of reach and the alternative is indefinite renting. The scheme was explicitly designed for this group, and the eligibility rules reflect that — though it is no longer restricted exclusively to first-time buyers.

Since April 2021, the UK Government’s updated shared ownership model opened eligibility to existing homeowners who cannot afford to buy on the open market, though first-time buyers and current shared owners retain priority. Household income must be below £90,000 in London or £80,000 elsewhere in England. Military personnel and those with a registered disability also receive priority access under the scheme.

The deposit advantage hits hardest for this group. A first-time buyer saving for a 10% deposit on a £300,000 property needs £30,000. With a 25% shared ownership share and a 5% deposit, that number drops to £3,750. For someone earning £35,000 and saving £500 a month, the difference is roughly four years of saving — time that would otherwise be spent paying rent with zero equity return.

The catch: younger buyers who expect to relocate within three to five years face the full weight of the resale restrictions. The nomination period, the restricted buyer pool, and the leasehold obligations all become liabilities rather than trade-offs if mobility is a priority. Shared ownership rewards stability. It penalises short time horizons.

Shared Ownership in London and Across the UK

Shared ownership delivers the strongest financial case in London and the South East, where the gap between average earnings and average house prices is widest. In lower-cost regions, the calculus shifts — and in some areas, full ownership with a government-backed mortgage scheme may actually be cheaper overall.

According to the Office for National Statistics (ONS) housing affordability data (2023), the median house price in London is roughly 12 times median annual earnings. In the North East, that ratio drops to around 5.5. The wider the affordability gap, the more financial sense shared ownership makes as a bridge.

London shared ownership properties carry a higher income cap (£90,000 versus £80,000), reflecting the capital’s cost premium. Service charges in London also tend to be significantly higher — particularly on new-build flatted developments in zones 2-4, where annual service charges of £2,500-£4,000 are common. Buyers in London must stress-test their affordability against realistic service charge trajectories, not just the first-year figure quoted by the developer.

Outside London, shared ownership can still make sense in cities like Bristol, Brighton, Cambridge, and Manchester where affordability ratios run well above the national average. In areas where the house-price-to-earnings ratio is below 6, buyers should compare the total cost of shared ownership (mortgage + rent + service charge) against a standard 95% mortgage under the Mortgage Guarantee Scheme — the latter may actually produce lower monthly outgoings and no leasehold restrictions.

What Martin Lewis and Real Owners Say

Martin Lewis’s MoneySavingExpert verdict on shared ownership is measured: useful for specific buyers, but not universally good. His team’s analysis highlights the rent-plus-mortgage double payment structure as the scheme’s core tension, and warns that staircasing costs can exceed expectations when property values rise between tranches.

Reddit communities — particularly r/UKPersonalFinance and r/HousingUK — carry a notably more sceptical tone. Recurring complaints include unexpected service charge increases, difficulty selling within the nomination period, and frustration with housing association responsiveness on maintenance issues. One widely upvoted thread from 2024 summarised it bluntly: “It takes all the upsides out of owning.”

That said, forum sentiment skews negative because satisfied owners rarely post. A BBC investigation in 2024 documented genuine cases of shared owners feeling “trapped” — but also noted that many buyers who understood the scheme’s limitations upfront reported satisfaction with their purchase. The deciding factor in nearly every positive account was thorough due diligence before exchange, particularly around service charge history and lease terms.

Frequently Asked Questions

What are the main disadvantages of shared ownership?

The biggest drawbacks are the layered monthly costs, leasehold restrictions, and resale difficulty. As a leaseholder, you pay 100% of repair costs despite owning only a fraction of the property. Service charges — set by the housing association — can rise unpredictably, and selling requires navigating a nomination period that limits your buyer pool to other scheme-eligible buyers.

Is shared ownership cheaper than renting?

Not always. On a £280,000 property with a 25% share purchased, total monthly outgoings — mortgage, subsidised rent, and service charge — typically reach around £1,041, compared to roughly £1,200 for equivalent private rent in the same area. The saving is modest, and the financial advantage comes primarily from equity accumulation rather than lower monthly costs.

Can you lose money on shared ownership?

Yes. If property values fall, your share loses value just as any owned asset would. Escalating service charges can erode affordability over time, and a forced sale during the housing association’s nomination period — typically eight weeks — may result in a lower sale price due to the restricted buyer pool. These risks broadly mirror those of full ownership rather than being unique to the scheme.

What happens when you sell a shared ownership property?

The housing association has first right of refusal for a fixed nomination period — typically eight weeks — during which it can find a qualifying buyer before the property reaches the open market. All buyers must meet shared ownership eligibility criteria, which significantly narrows demand compared to a standard freehold sale and can extend time on market, particularly in slower regional markets.

Does staircasing always make financial sense?

Not automatically. Each staircasing tranche is priced at current market value, meaning rising property prices increase the cost of each step. In a fast-appreciating market, delaying staircasing makes full ownership progressively more expensive. Buyers should model the cumulative rent paid during the staircasing period against projected share price increases before assuming staircasing is the cheapest route to outright ownership.

Is shared ownership freehold or leasehold?

Almost always leasehold. Shared ownership properties are sold on long leases — typically 99 or 125 years — granted by the housing association. Even shared ownership houses are usually leasehold, unlike houses purchased on the open market which are generally freehold. The lease governs service charges, ground rent obligations, and what alterations you can make without the housing association’s written consent.

Do you pay council tax on shared ownership?

Yes, in full. Regardless of whether you own 25% or 75% of the property, you are liable for 100% of the council tax band applicable to that address. There is no reduction or exemption linked to the size of your owned share. Standard council tax discounts (single-person discount, student exemption) still apply as they would for any other household.

Is shared ownership the same as rent to buy?

No. Shared ownership and rent to buy are distinct government-backed schemes. Under shared ownership, you purchase a share immediately and pay rent on the remainder. Under rent to buy, you rent at a discounted rate (typically 80% of market rent) for a fixed period — usually five years — while saving for a deposit, with the option to buy at the end. Rent to buy involves no equity ownership during the rental phase.

Is shared ownership a housing association scheme?

Yes. Shared ownership properties are developed and managed by Homes England-registered housing associations (also called registered providers). These associations build or acquire the properties, sell shares to qualifying buyers, retain the unsold portion, and collect rent on it. The housing association also sets service charges, manages communal areas, and controls the nomination period when you sell.

Is shared ownership halal?

Conventional shared ownership involves a standard interest-bearing mortgage, which is not compliant with Islamic finance principles. However, several UK lenders now offer Islamic finance alternatives structured as diminishing musharakah — a partnership arrangement where the bank and buyer jointly own the property, and the buyer gradually purchases the bank’s share through rental payments rather than interest. Buyers seeking Sharia-compliant options should contact specialist Islamic mortgage providers directly.

Can you buy to let a shared ownership property?

No. Shared ownership properties cannot be used as buy-to-let investments. The lease requires you to live in the property as your primary residence. Subletting is prohibited without explicit written permission from the housing association, and permission — if granted at all — is typically limited to short-term lettings under exceptional circumstances such as temporary work relocation.

Is shared ownership government backed?

Yes. Shared ownership is a government-backed affordable housing programme administered through Homes England in England. The scheme’s eligibility criteria, income caps, and model lease terms are set by central government policy. Housing associations that deliver shared ownership must be registered with the Regulator of Social Housing, providing regulatory oversight that private-sector leasehold arrangements do not carry.

Is shared ownership part of Right to Buy?

No. Shared ownership and Right to Buy are entirely separate schemes. Right to Buy allows council tenants to purchase their rented council home at a discount. Shared ownership is available to qualifying buyers purchasing newly built or resale properties from housing associations. The two schemes have different eligibility criteria, different pricing structures, and different legal frameworks.

Is shared ownership only for first-time buyers?

No, not since the 2021 reforms. While first-time buyers receive priority, the scheme is now open to existing homeowners who cannot afford to buy on the open market, as well as current shared owners looking to move. Military personnel qualify regardless of previous ownership status.

Is Shared Ownership Worth It? The Bottom Line

Shared ownership can be worth it — but only when three factors align: you face a genuine affordability gap in a high-cost area, your long-term plans are stable enough to justify the leasehold commitment, and you’ve stress-tested the local resale market. For buyers in London and the South East with limited deposits, the scheme offers a real route onto the ladder that renting simply cannot match.

The risks are equally real. Escalating service charges, the housing association’s nomination period, and the rising cost of staircasing each tranche at current market value can erode the financial case faster than most buyers anticipate.

Before committing, speak to an independent mortgage broker with direct shared ownership experience — not a generalist. A specialist broker can model your total monthly outgoings, stress-test a staircasing timeline, and compare the scheme honestly against alternatives like the Lifetime ISA or Mortgage Guarantee Scheme for your specific situation.